Iran and the Economy: The Danger Isn’t the Shock. It’s the Duration.

Randolph Bourne said war is the health of the state. Fine. Then let’s say the other part out loud: war is a disease in the economy.

That is the real economic question hanging over the Trump administration’s war on Iran. A short, bounded conflict can be absorbed. A prolonged one doesn’t just raise the odds of a recession. It can lower the economy’s speed limit by diverting real resources, depressing investment, and extending a politics of permanent emergency. We’ve seen that movie. We even gave the middle act a name: secular stagnation.

War Costs Don’t End with the Price of Oil

The first thing markets do in a Persian Gulf war is stare at crude oil prices. Energy is still the quickest way geopolitics shows up in household budgets and corporate margins. This week, we saw a dynamic daily: when oil surged, stocks plunged. When oil prices eased, stocks rose. But oil is only the most visible channel.

A trader works on the floor of the New York Stock Exchange on Thursday, March 5, 2026. Oil prices surged amid concerns of a prologued Iran war. (Michael Nagle/Bloomberg via Getty Images)

The deeper channel is the one that doesn’t come with a flashing price screen or a ticker running across financial television: the diversion of real resources. War pulls scarce inputs—high-skill labor, industrial capacity, managerial attention—into the war apparatus and its domestic support ecosystem: procurement, intelligence, logistics, contracting, compliance, security, and the “temporary” architecture that has a habit of becoming permanent.

Keynes put the essence of this in a sentence that ought to be printed on every war appropriation: “Every use of our resources is at the expense of an alternative use.” In wartime, he wrote, the “cake” is effectively fixed: if we fight better, we don’t get to eat more. That is the part of war economics that gets lost when we talk only about the budget line. War doesn’t merely spend money. It redirects the country’s scarce capacity, and the civilian economy becomes smaller than it otherwise would have been because the “alternative use” never happens.

Milton Friedman, from a very different tradition, reinforces the same core point from another angle. He argued that inflation is not an inevitable consequence of war; it depends on how the war is financed. That’s useful because it separates two questions people constantly confuse. A country can finance war without an immediate inflation blowout. But it still pays the basic price Keynes described: foregone civilian output and foregone investment. Even when the CPI behaves, the opportunity cost is real.

The Economics in One Unglamorous Number

If war spending reliably made the economy richer, you’d expect defense outlays to generate big multipliers. But the economic research points the other way.

Robert Barro, the Harvard economist best known for work on growth and fiscal policy, and Charles Redlick tried to answer a simple question with hard data: when Washington ramps up defense spending, how much extra economic output do we actually get? They measure what economists call the “multiplier”—the ratio of the change in GDP to the change in government spending. If the multiplier is one, a dollar of defense spending adds roughly a dollar to GDP. If it’s less than one, the government is buying real stuff—labor, steel, fuel, factory capacity—but total output rises by less than the amount spent because other activity is being pushed aside.

Barro and Redlick’s estimates for temporary defense spending come in well below one: roughly 0.4 to 0.5 on impact and still below one over a couple of years. That is a polite academic way of saying war spending displaces civilian production, and what tends to get displaced is precisely what you’d least like to sacrifice if you care about living standards five years from now: private investment.

That’s the heart of the long-war danger. The economy can look busy while quietly investing less in the machinery, infrastructure, and innovation that raise productivity. This is “crowding out” without the interest-rate morality play. Interest rates can stay low, and you can still get crowded out in the only sense that ultimately matters. Real resources are finite.

Distortion Is the Rule, Not the Exception

If you want to see what “diverted production” looks like when it’s real, you don’t need economic theory. You need a history book.

During World War II, war-related production in the United States exploded. Economic historians note it rising from a sliver of national output before the war to something like two-fifths of GNP at the peak. That wasn’t a stimulus program, even if it looked like one in the headlines. It was the economy being repurposed. World War I did the same thing, at a smaller scale but with the same logic: production shifted from civilian to war goods, labor was drafted or redirected, and the financing mix—taxes, borrowing, money creation—created its own aftershocks.

View of the production line of B-24E Liberator bombers being assembled at the Ford Motor Company’s massive Willow Run plant in Ypsilanti, Michigan, during World War II. (PhotoQuest/Getty Images)

You don’t have to romanticize mobilization to learn the lesson. The lesson is that when war becomes prolonged, the economy gets reorganized around it. And reorganizing an economy has consequences that persist long after the first headlines fade. When the economy is operating well below capacity, with lots of slack and under-employed labor, mobilization can lift output. That’s the basic World War II story. But when unemployment is low and output is already cranking—as it is now—the effect is mostly reallocation rather than expansion: more guns, less butter, and a thinner future.

Modern research has started to capture this reallocation cost more directly, not just in GDP aggregates, but in bottlenecks, relative prices, and the friction of converting civilian industry into war production. The more specialized and complex the economy is, the more painful that repurposing becomes. That’s another way to say “malinvestment” without turning it into a slogan: resources and capabilities get pushed into lines of production that do not compound into broad prosperity. The war machine devours what should have been our wealth.

Iraq’s Bill Wasn’t One Number. It Was a System.

The Iraq war is useful as an analogy not because it was the same conflict, but because it shows how quickly costs stop being a line item and become a condition.

On the war’s tenth anniversary, the Costs of War project at Brown University estimated Iraq’s ultimate price tag at at least $2.2 trillion once you include long-run obligations like veterans’ care and interest. A decade later, the twentieth-anniversary update pushed the total expected budgetary cost above $2.89 trillion, with a large share of the remainder coming from obligations that stretch out for decades.

Those totals, however, don’t fully capture what makes a long war economically corrosive. The most damaging part is often the part that doesn’t show up as “war spending” at all: postponed investment, diverted talent, a shortened horizon, and a private sector that limps rather than strides into the future.

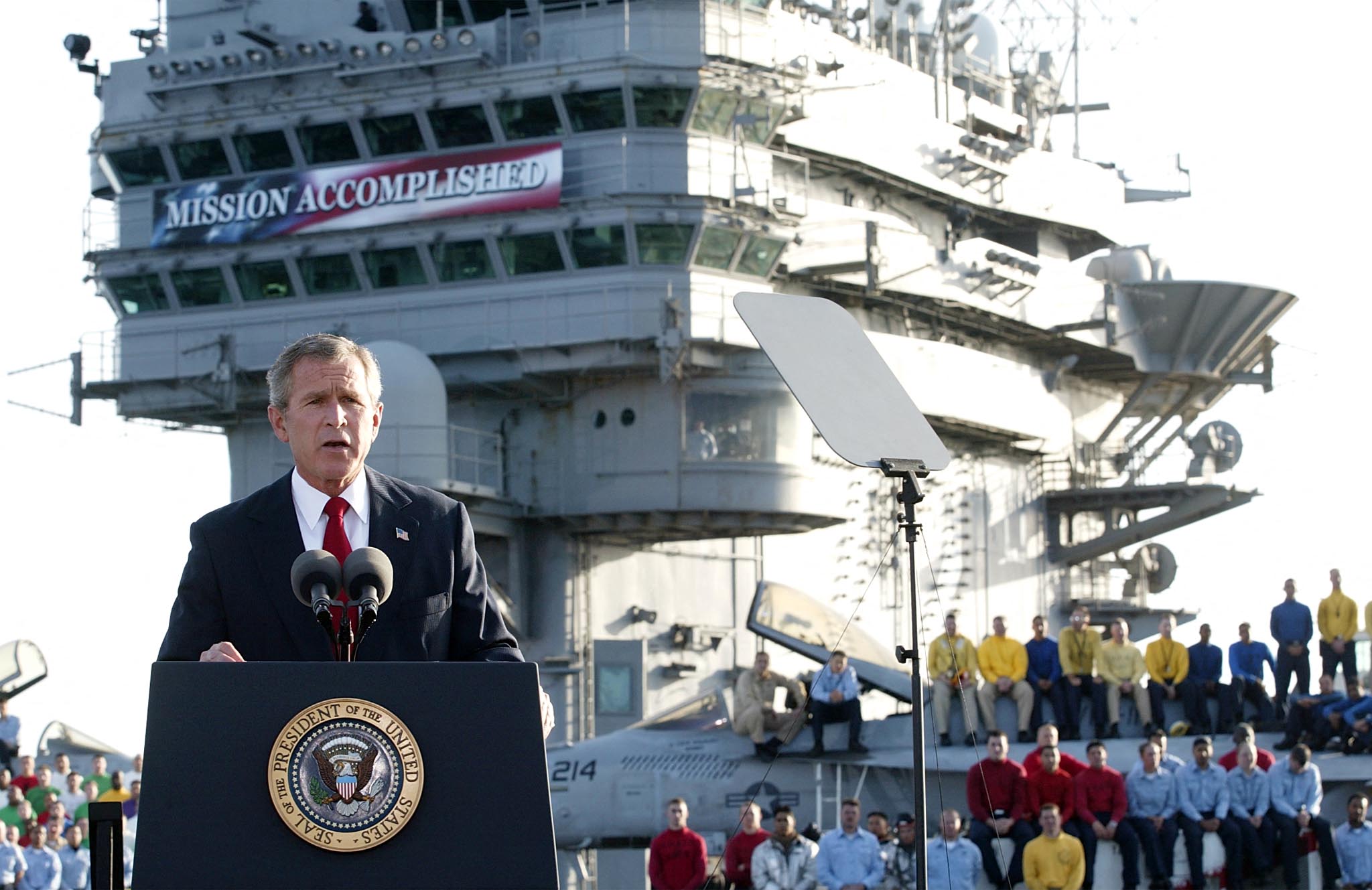

That’s how you can have a decade when interest rates are low, the central bank is trying to coax growth back to life, and yet the economy still feels like it is dragging a chain. It’s how you go from mission accomplished to secular stagnation.

President George W. Bush addresses the nation aboard the nuclear aircraft carrier USS Abraham Lincoln on May 1, 2003, in front of a banner declaring “Mission Accomplished” after the invasion of Iraq. (STEPHEN JAFFE/AFP via Getty Images)

In the years that followed our invasion of Iraq, productivity growth slumped, and wage gains followed it down. That slowdown is usually pinned entirely on the housing bubble and the financial crisis. But the drag of the Forever Wars was a serious contributor to what became known as secular stagnation.

The Pottery Barn Rule and the Economics of Mission Creep

Iran is especially dangerous because it offers so many on-ramps that look like off-ramps. Even if the goals are clearly defined at first—destroy Iran’s nuclear capacity, cripple its military, break the regime’s ability to project power—the fog of war tends to blur things. There is always a “just.” Just protect shipping lanes. Just hit proxies. Just restore deterrence. Just stabilize. Just help rebuild institutions. Just one more month, one more quarter, one more year.

Then comes the rhetorical device that turns mission creep into moral obligation: the so-called “Pottery Barn rule”—if you break it, you own it. Peter Schweizer’s point deserves emphasis: Trump is rejecting that nation-building reflex. Destroy the threat; don’t sign up to rebuild the society.

That rejection matters economically as much as it matters strategically because the “Pottery Barn rule” is a machine for creating duration. And duration is what turns a conflict from a shock into a structural drag.

Plumes of smoke rise following explosions in Tehran on March 3, 2026, after Iran’s Supreme Leader Ayatollah Ali Khamenei was killed in joint U.S. and Israeli strikes on February 28, sparking a wave of retaliatory missile strikes from Iran across the region. (Negar/Middle East Images/AFP via Getty Images)

It’s also worth remembering that this “rule” is not ancient wisdom. It’s a relatively recent slogan that acquired the status of doctrine mostly by repetition. Worse, the retail story behind it—the famous “you break it, you bought it” policy—was itself an urban legend. We laundered mission creep through a catchy metaphor, and then acted surprised when rebuilding turned into occupation, and occupation turned into a war with a decade-long economic shadow.

War Will Not Make America Great Again

A short war hurts. A long war changes what kind of economy we have and what kind of country we are.

If Iran stays a bounded military problem, the U.S. economy can adjust. If it becomes a prolonged political project, the cost won’t just be budgetary. It will be structural: weaker investment, weaker productivity growth, and a private economy that learns to live with diminished expectations.

War is the health of the state. It’s also the sickness of the economy. Sometimes what doesn’t kill you just keeps you weak.

{kind=link}